A mobility operation in a tourist city looks, from the outside, like a standard case of regional ride-hailing. Same platform, similar drivers, the same sedan. What changes, fundamentally, is who is on the other side of the screen: not a resident who knows the city and has repeatable mobility patterns, but a visitor who arrives without local references, who may leave tomorrow, who values certainty over price, and who in many cases won't return. That difference in passenger profile isn't an operational footnote — it's the central reason to build a different product model from day one.

This post is for operators already running in tourist destinations — colonial cities, beach towns, places with seasonal or year-round visitor flow — or evaluating a tourist city as a next market. The argument isn't that the standard secondary-city model is wrong; it's that applying it without adaptation produces atypical unit economics, driver retention problems in low season, and a passenger experience that fails to capture the highest-value segment in that kind of market.

Tourists and residents ask for different things

A resident who uses a mobility app has history: they know what the usual route costs, may have a preferred driver if the platform allows it, and don't stress about the commute fare they've paid a hundred times. A tourist has none of those references. They don't know whether $8 USD to the hotel is expensive or reasonable for that city. They don't know which driver on the platform is reliable. And they carry a higher cost of uncertainty: if the app fails in an unfamiliar city, they're stranded without local alternatives. That's why tourists don't optimize for price — they optimize for certainty. That difference in motivation has direct consequences for product design, fare structure, and acquisition channel.

The second difference is the time horizon of value. A recurring resident in a regional operation represents between $180 and $430 USD in 12-month LTV — as detailed in the unit economics post. A tourist visiting once has a LTV of essentially zero beyond the trips they take on that visit, unless they're a frequent visitor or the platform has between-visit retention tools. That doesn't make the tourist low value — their individual ticket can be 2x or 3x a resident's if the route justifies it. It means the tourist's value metric isn't LTV but maximum ticket per trip and the likelihood they recommend the platform to other visitors.

High season isn't just more of the same

In a tourist city, high season isn't just more residential demand — it's an overlay of two demand types with completely different profiles. Residents maintain their usual patterns: commuting, visiting family, running errands. Tourists add an entirely new demand layer with different routes, schedules, and behaviors: airport transfers timed to the flight calendar, visits to zones residents rarely frequent, and late-night departures from restaurants and bars in areas the platform didn't treat as priority coverage. A platform calibrated only for residential demand enters high season without drivers positioned in tourist demand zones, with fares that don't reflect the longer routes to the resort or the waterfront, and without the advance booking flow that tourists require for airport transfers.

Preparing for high season in a tourist city must begin six to eight weeks out, not six to eight days. That means mapping tourist-specific demand zones — the airport, major hotels, the most-visited beaches or attractions, the historic center — and identifying which drivers have availability for those routes with the right vehicle and presentation standard. It also means defining a specific fare structure for the highest-ticket tourist routes that incorporates extended waiting times and real route distances. Tourist demand in high season is predictable enough to plan for; the only reason most operators manage it reactively is that they never established a preparation process from the start.

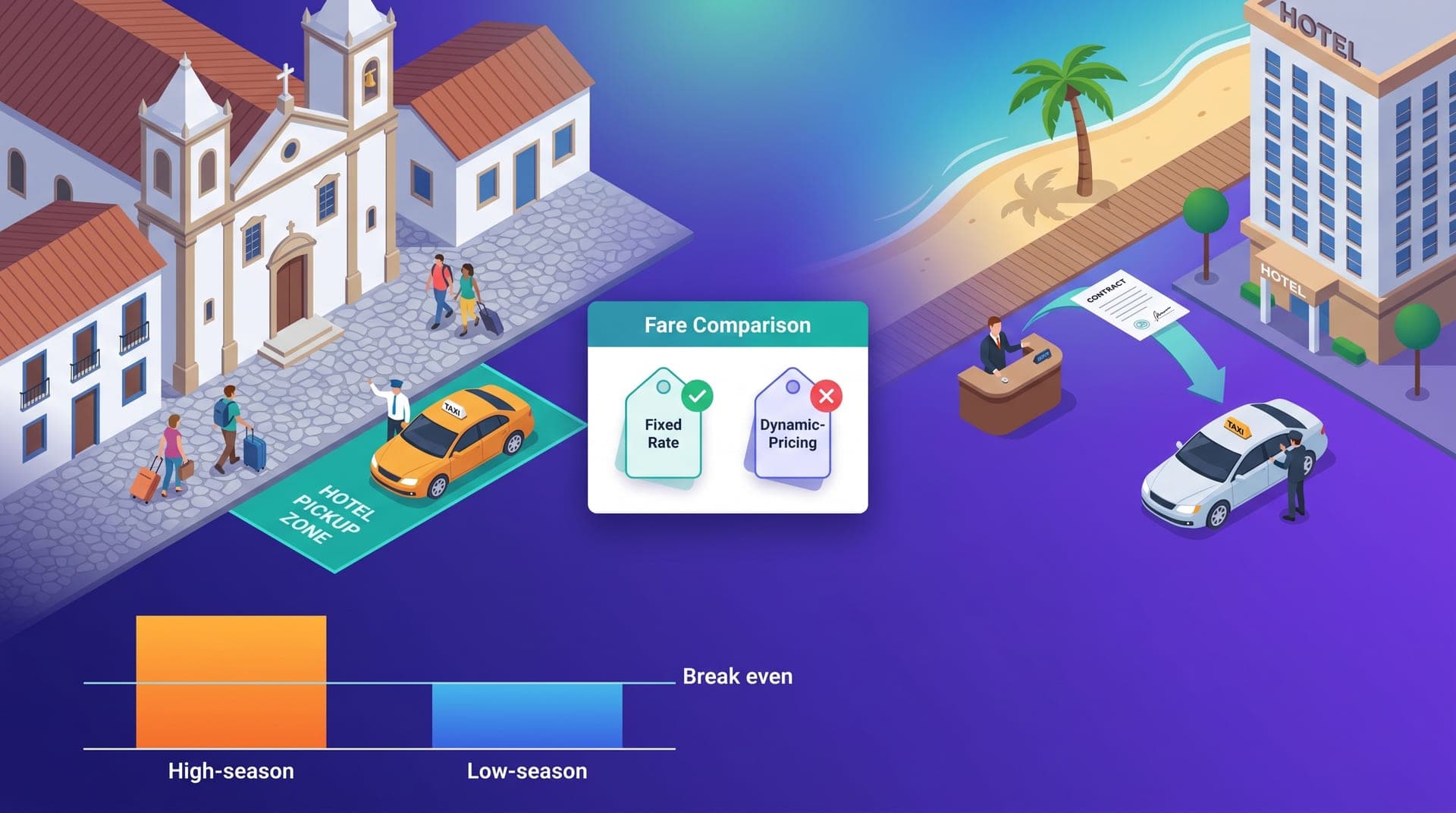

Why fixed fares dominate in tourist destinations

Dynamic pricing in a residential city has two simultaneous effects: it pulls drivers toward high-demand zones and signals to the passenger that supply is scarce. The resident passenger knows that context — it's Friday night, there's surge — and either accepts the multiplier or waits. The tourist has no such context. They see a 2.1x multiplier the first time they open the app in an unfamiliar city, can't tell whether that's normal or a scam, and close the app to find a street cab. That scenario, which in a residential city produces one cancellation and one complaint, in a tourist city produces a TripAdvisor review that the next visitor searching for transport reads before arriving.

Fixed rates by route are exactly what tourist passengers need — and what an operator can offer without sacrificing margin when routes are priced correctly. A fixed fare from the airport to the central hotel district, from the hotel to the dining area, from the historic center to the waterfront — published in the app and at the hotel desk — communicates certainty before the passenger makes their first request. That certainty carries a premium that tourists assign but regular residents don't, and that premium allows the operator to set fixed fares with more generous margins than they'd apply to the same route within standard dynamic pricing.

The airport and hotels as the model's backbone

The airport in a tourist city isn't an additional service — it's the revenue model's backbone. A tourist passenger arriving at the local airport has one immediate need and zero local references: reliable transport to the hotel. If the platform isn't visibly present — with a working app and a driver waiting for passengers with advance bookings — that passenger takes the hotel desk transfer or the taxi line. If the platform is there and the experience is good, the passenger has the app installed, the driver rated five stars, and every subsequent trip of that visit — hotel to beach, beach to restaurant, restaurant to bar — available to the platform. The airport isn't the most frequent trip; it's the trip that determines whether the subsequent ones happen on the platform or somewhere else.

Hotel contracts are the second piece of the core. An 80-to-150-room hotel in a tourist destination manages dozens of passengers with transport needs throughout the week. The hotel concierge recommends transport multiple times daily. If the operator has an agreement with the hotel — agreed fares, an identified driver, a confirmation mechanism — the concierge recommends the platform by default, not because the technology is superior but because the service is predictable and the operator is someone they can rely on when a guest has a problem at 2 a.m. A single contract with a hotel of that size can represent $1,800 to $4,500 USD in monthly recurring revenue, with zero acquisition cost after the first signed agreement.

Low season: the risk the model must anticipate

Low season in a tourist city isn't a temporary dip — it's the test of whether the business model is sustainable or whether the operator built an operation that only works four or five months a year. In destinations with sharp seasonality, total demand can fall between 45% and 70% during the lowest tourist-flow months. An operation that never built solid residential demand — because chasing tourism was easier in high season — arrives at low season without the recurring passenger base that covers fixed costs. Drivers who earned $4.50 to $6.00 USD per active hour in peak season now earn $1.80 to $2.40 USD and start disconnecting from the platform. When the next high season arrives, the operator has no experienced service drivers and must rebuild the fleet from scratch.

The response to low season isn't to scale back and wait — it's to build residential demand during high season. This requires the operator to treat resident passengers with the same care as tourists: competitive fares for everyday routes, drivers available during regular commute hours, and an active resident acquisition channel that doesn't depend on tourist flow. An operation that in high season is 60% tourists and 40% residents can sustain its cost structure through low season with the resident base if the unit economics of that segment are sound. A 90% tourist operation has no such cushion and must make a full reactivation push every year.

The metrics that shift in a tourist market

Unit economics in a tourist market aren't simply higher than in a residential one — they have a different shape. Average ticket is higher, but support cost per trip is also higher because tourists generate more first-time incidents, more questions, and higher expectations for immediate response. Tourist-channel CAC is higher than residential-channel CAC because it requires physical presence at the airport and active hotel relationships, not just digital marketing. And monthly break-even in low season may require twice the daily trips as high season if average revenue drops with dynamic pricing — that calculation must be done with data from both seasons, not just the annual average.

Metrics that behave differently in a tourist city versus a standard secondary market:

- Effective tourist CAC is higher than resident CAC because it includes the time and relationship cost of establishing airport presence and hotel agreements before they generate returns

- Frequent-tourist LTV — a visitor who returns two or three times a year — can exceed that of an occasional resident if the platform has between-visit retention tools such as reminders before the next flight

- Cancellation rate in high season can triple that of a residential market if dynamic pricing activates without prior communication — that number needs weekly monitoring during the peak period

- Driver active-hour earnings in high season can run 30% to 60% above the retention threshold, but fall below it in low season if residential demand hasn't been built alongside the tourist base

- Average ticket in a tourist market typically runs 1.5x to 2.5x that of an equivalent residential market, but per-trip margin doesn't scale proportionally because tourist trips carry higher support costs

- Monthly break-even in low season may require twice the daily trips as high season if average fare drops with dynamic pricing — that calculation must be done with both-season data, never with the annual average

The first summer I went all-in on tourists: airport, hotels, beaches. The numbers were incredible. In November the tourists left and I had fourteen drivers and no passengers. It took me three months to understand I should have been building the local base while the tourist flow still gave me the margin to invest in that segment.

A tourist city that works profitably for a mobility platform isn't the one that captures the most trips in high season — it's the one that builds a two-season model generating revenue in both phases of the year. That means designing the product with two passenger profiles in mind from the start: the tourist who pays more for certainty and won't return if the experience fails, and the resident who pays less but generates the demand base that sustains the cost structure during low tourist-flow months. The platform, fares, and acquisition channels must be calibrated for both — not for one or the other depending on the season.

Operators who succeed in tourist markets share a pattern: they treated the airport and hotels as the primary acquisition channel for the tourist segment, but invested the first high season in simultaneously building resident demand. When low season arrived, they had 40% to 50% of residual demand covered by recurring residents — enough to keep the fleet active and drivers on the platform without permanent loyalty incentives. That threshold doesn't require massive scale: in a tourist city of 80,000 to 150,000 residents, 300 to 500 recurring passengers represent between 1,800 and 4,000 monthly trips in low season — enough volume for the operation to be self-sustaining while the next tourist peak approaches.