Most regional ride-hailing operators in LATAM solve the hard part of landing a corporate client: the prospecting, the proposal, the price negotiation, and the service terms. Then, in the first or second month of operating with that client, the contract runs into complications from something that never comes up in any sales conversation: the invoice. The company requests a document with the correct fiscal data, in the format required by local tax authorities, with line items broken down according to their purchasing department's internal catalog, delivered within the billing cutoff that lets them close their month-end accounting. The operator delivers it four days late, with the wrong RFC or NIT, without the reference number accounts payable needs to match it to a purchase order. Finance escalates to the executive who approved the contract. That executive calls the operator to sort it out. And the contract that was supposed to be the first of eight corporate accounts becomes the internal example that executive uses to explain why switching transport providers is more friction than it appears.

This article is for operators with one to five active corporate contracts, or who expect to sign their first corporate agreements in the next ninety days. The focus is not on selling the contract — that belongs to the commercial process and the service value proposition. The focus is the billing process that happens after the signature: what to configure before issuing the first corporate invoice, what the differences are between fiscal frameworks in Mexico, Guatemala, and Colombia that have direct operational impact, and what errors cause a commercially successful contract to end for administrative reasons the operator could have prevented with a week of preparation.

Why the invoice decides whether the contract survives the first quarter

Corporate accounts in ride-hailing have a different decision structure than individual passenger accounts. A passenger decides whether to return based on the trip experience: wait time, driver behavior, relative price. A corporate client makes that same renewal decision based on the experience of a department that never rode in a vehicle: finance or accounts payable. If billing arrives correct, on time, and in the expected format, finance generates no complaints and the contract renews with almost no deliberation. If billing produces a discrepancy — a wrong RFC in Mexico, an incorrect NIT in Colombia, a line item description that doesn't match the company's purchasing catalog — the resolution process involves people's time in two separate organizations and creates the friction that eventually triggers a provider change.

Corporate payment cycles in LATAM range from 30 to 60 days for most mid-size companies, with some larger organizations operating on 90-day cycles. That means the first actual payment on a contract signed in January may not arrive until March or April. For the operator, that period is a complete stress test of the billing chain — and if there is an error in the first month's invoice, payment is delayed until the error is corrected, which can extend the collection period to 90 or 120 days with direct impact on operational cash flow. The technical error costs a week of back-office time to resolve. The financial effect of that error can last two or three months.

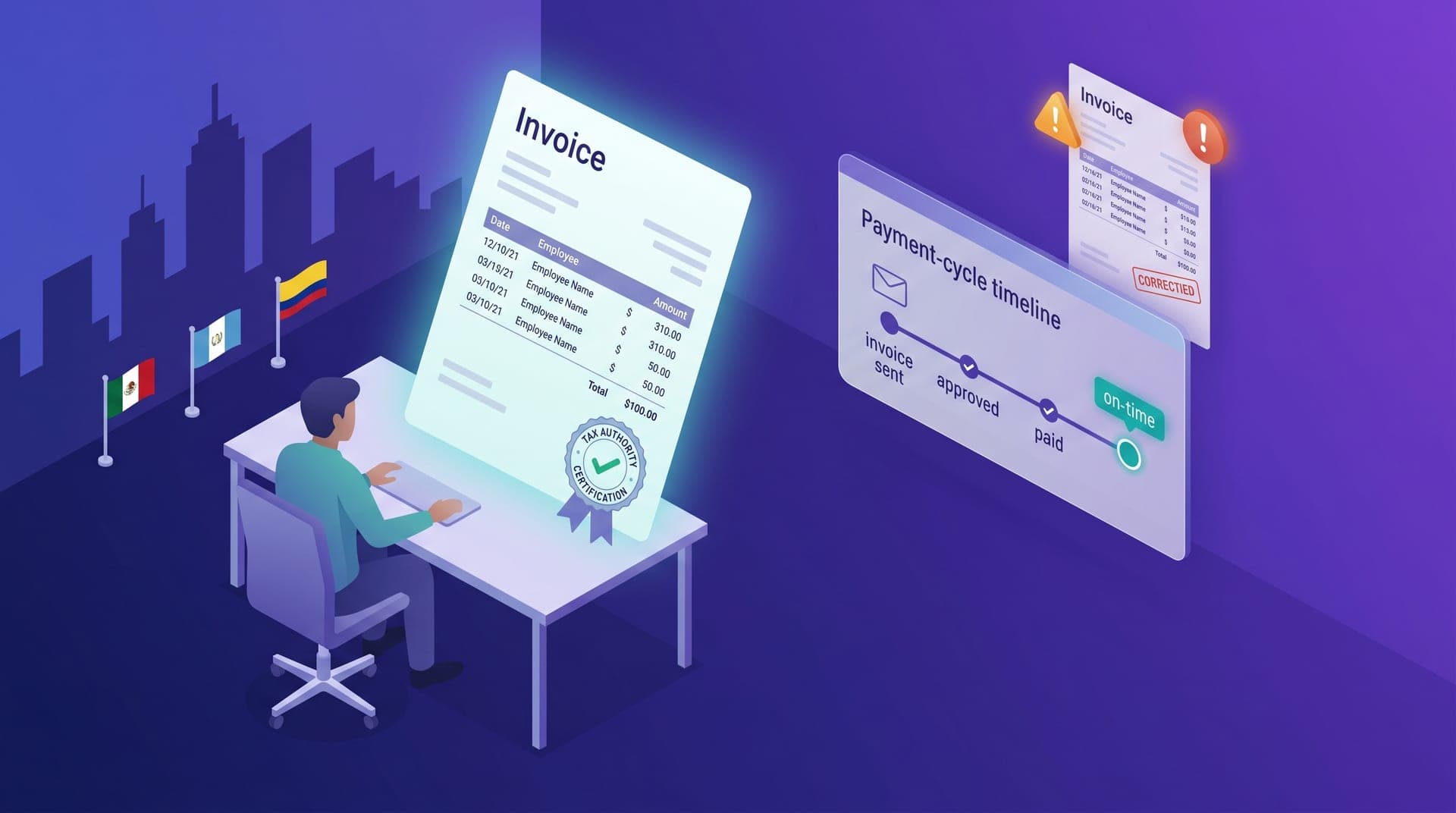

The level of detail finance requires — and that no contract specifies

Corporate ride-hailing contracts are typically structured as monthly credit accounts: the company authorizes trips during the month and receives an invoice at period close for the total rides taken. But that total is rarely sufficient on its own. Most finance departments in mid-size companies require a breakdown by employee, by day, by project, or by business unit — depending on how the company classifies transport spend in its accounting system. An operator who issues a monthly invoice with a single line of 'Transport services — 52 trips — $11,300 MXN' will receive a clarification request with a list of what accounts payable needs to see before releasing payment. That level of detail has to exist in the platform system before the first corporate trip happens — it cannot be reconstructed after the fact with the granularity the client requires if the data was not captured from the start.

The minimum platform configuration needed before activating the first corporate account includes an employee reference or cost center field per trip — not as an optional field but as a required one for trips in corporate mode — and the ability to generate a report filterable by those references, exportable in the format the client's purchasing department works with. Without that structured data foundation from the first trip, the operator can deliver the service correctly but cannot produce an invoice with the level of detail the client needs to process it without escalating to their technology or procurement team.

What to have ready before issuing the first corporate invoice

There is a set of data and integrations the operator needs to configure in advance — not after the first month-end close when the client requests the invoice and the process stalls. That preparation is not technically complex on most modern ride-hailing platforms, but it requires an active conversation with the client's finance team before service starts, not only with the commercial executive who signed the contract.

The information to obtain and configure before the first corporate trip includes:

- Client fiscal data validated directly with their finance team — RFC with homoclave in Mexico, NIT in Colombia and Guatemala — not with the commercial executive who signed the contract

- Expected invoice format by jurisdiction: CFDI 4.0 with use code D10 or G03 in Mexico, FEL in Guatemala, DIAN electronic invoice in Colombia — each requires a distinct issuer configuration in the platform system

- Monthly billing cutoff and invoice receipt deadline for the client to process within their accounting close — if the client closes on the 5th and the operator delivers on the 10th, the invoice falls into the following period and collection is delayed 30 days

- Required breakdown level in the trip report: by employee, by project, or by business unit — and the platform field that captures that reference trip by trip from the moment of the request

- Purchase order number or requisition reference that must appear on the invoice for accounts payable to link it to the approved budget without additional back-and-forth

- Invoice delivery channel: direct email to the finance team, the client's vendor portal, or EDI system — vendor portals have additional format requirements the operator must verify before the first submission

- Name and direct contact for the accounts payable team — not the commercial executive — to resolve billing discrepancies without intermediaries who extend resolution time

CFDI, FEL, and DIAN: the fiscal differences that affect operations

The three electronic invoicing frameworks most relevant for ride-hailing operators in LATAM have distinct characteristics that directly affect the month-end closing flow. In Mexico, CFDI 4.0 (Comprobante Fiscal Digital por Internet) has required since 2022 that invoices include the RFC with homoclave of the recipient, validated against the SAT registry — making invoices issued with the generic public RFC (XAXX010101000) invalid for clients who need to deduct the expense. Stamping requires active integration with a PAC (Authorized Certification Provider), an external service the ride-hailing platform must have configured to issue fiscally valid documents. An operator issuing invoices in Mexico without PAC integration is generating documents the client cannot use for tax deduction and that the tax authority does not recognize as valid.

In Guatemala, FEL (Factura Electrónica en Línea) operates with real-time certification through the Guatemalan SAT's system: each invoice is certified online at the moment of the transaction, with an authorization code that forms part of the document. The difference from Mexico's CFDI is that FEL introduces a dependency on active connectivity with the SAT's servers at the time of issuance — something the operator must manage in the corporate trip closing flow. In Colombia, electronic invoicing under DIAN's framework has been mandatory since 2020-2022 for most productive sectors. The most frequent error in Colombian ride-hailing operations is issuing 'equivalent documents' — which are technically not DIAN electronic invoices — when the corporate client needs a valid invoice for VAT and income tax deduction. That distinction is not always obvious to the operator's operations team, but the client's finance department knows it precisely.

The two errors that cost the most corporate contracts — and neither is technical

The error that costs the most corporate contracts is not the technical one — the wrong RFC or an outdated invoice format — but the timing error. Mid-size companies in LATAM have accounting close cycles with rigid dates: if the invoice doesn't arrive before the 5th of the following month, it doesn't enter the prior period and finance processes it in the next month's cycle, extending the collection period by 30 to 60 additional days. An operator who consistently delivers invoices on the 10th is financing the client's operations with their own working capital for an avoidable period. After two or three cycles with this pattern, the client starts evaluating alternatives — not because the service is poor but because the administrative process creates friction their finance team is not willing to sustain indefinitely.

The second most frequent error is recipient data. In Mexico, the 2022 fiscal reform that made the RFC with homoclave mandatory in CFDI 4.0 invalidated invoices issued with the generic RFC for clients who could deduct the expense. Operators who did not update their issuance flow after that date issued months of invoices the client could not use for tax deduction, which had to be reissued with the corresponding payment delay. In Colombia, an equivalent error occurs when the operator doesn't have the client's correct NIT or issues the wrong document type for the transaction. These errors have direct technical solutions, but the commercial damage — a client who was slow to pay while the problem was resolved and who now evaluates available alternatives more carefully — is harder to reverse than the fiscal correction.

The first corporate contract I lost wasn't over price or availability — it was because our invoice arrived on the 12th and their finance team closed on the 5th. After three months, the accumulated unbilled trips reached 46,000 pesos. The executive who had approved the contract stopped responding. By the time I understood that client's close cycle, it was already too late to reactivate the account.

How friction-free invoicing becomes a retention advantage

Correct corporate billing is not just a compliance obligation — it is a differentiator in a market where most small operators don't have a robust B2B invoicing process. A company that has gone through the experience of correcting invoices, waiting for clarifications, and managing discrepancies with a transport provider will actively value the operator who delivers the right document, on time, with the level of detail finance needs to process it without follow-up questions. That is the kind of experience that converts an active corporate account into a reference for the next contract.

The concrete operational advantage is frictionless renewal. A corporate client whose finance team receives no complaints about the transport provider's billing has no active reason to evaluate alternatives when renewal time comes. The decision becomes a non-decision: no one has to renegotiate price or justify switching because the process runs without anyone having to manage it. In a market where landing a new corporate client costs two to five times more than retaining an existing one, friction-free invoicing has a direct financial return that operations teams tend to underestimate because it happens silently, in the moment the invoice arrives correctly and no one calls to ask about anything.

Corporate electronic invoicing in LATAM is not a uniform process: each country has its own framework, tax authority, and validity periods. For an operator with clients across more than one market, that means distinct configurations in each jurisdiction, with different certifiers or PAC providers, different invoice formats, and different close cycles that the billing system must manage independently. The right moment to resolve that complexity is not when the first corporate client requests a clarification — it is before signing the first contract.

Operators who treat corporate billing as a back-office function to be resolved on the fly will find that the cost of errors — in team time, delayed cash flows, and lost contracts — frequently exceeds the cost of having configured it correctly from the start. Those who treat it as part of the product the corporate client evaluates when deciding whether to keep the contract will build a portfolio of accounts with higher retention rates, more predictable collection cycles, and a growing number of active references that reduce the acquisition cost of subsequent contracts.